The third quarter of 2023 presented speed bumps in financial markets. Across global equity markets we saw stocks pull back and at the same time bond yields moved higher. Although the Federal Reserve held their rate steady at the much-anticipated September meeting, the narrative of higher rates for longer coming out of the meeting has weighed heavily on markets. This combined with a looming US government shutdown, concerns about the US market being overvalued and economic stagnation overseas has many investors squeamish about the future.

If we look beyond the headlines though, there are still pockets of opportunity and reasons to be optimistic about the outlook. Let’s unpack some of the key headlines about markets and investing of late.

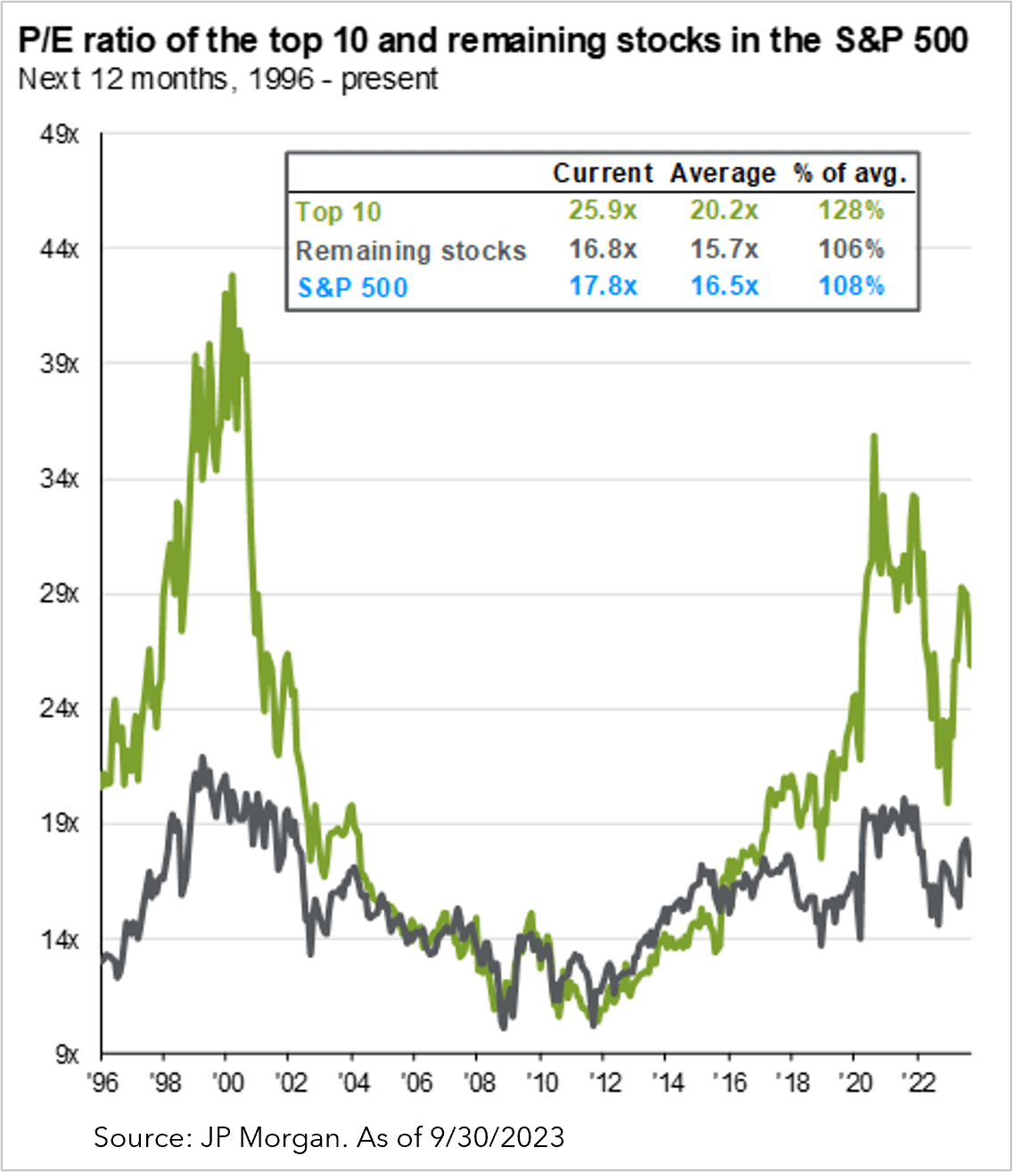

Are US stock market valuations too high?

If we look at the overall price of the S&P 500 versus the expected earnings of the index for the next 12 months and compare that to the average ratio for the index over the past 25 years, valuations appear high. However, what is not captured by the headline number is that the high valuation of the S&P 500 index is largely driven by the top ten stocks within the index. The median stock in the S&P 500 is up only 5%1 on a year-to-date basis and if you exclude the top 10 stocks, the valuation of the remaining stocks is a much more reasonable 16.8x.

Taking this a step further, there are stocks beyond the S&P 500 that are also part of the US market i.e., mid cap and small cap stocks and those stocks are more reasonably priced, not only compared to the S&P 500, but also compared to their own 20-year average valuation.

Price is a critical factor in future expected returns and generally when valuations are lower, returns in the future tend to be higher. While the headline numbers may suggest that the US market valuation today is high, this headline number hides the dispersion of stocks within the market and should not be construed to mean that future expected returns are lower for all stocks or the market itself is doomed to produce poor returns.

Should international markets be avoided?

The key question though is how much of the bad news is already priced in? It is possible that expectations for growth are already low enough that whatever bad news comes next has less of an impact on European stocks. From a valuation standpoint international developed stocks are not only trading at a discount relative to US stocks, but also trading at a discount relative to their own historical averages. Dividend yields on international stocks are almost 2%2 higher than US stocks, arguably making them a bargain.

Are money market funds and Treasury bills the best place to park your money?

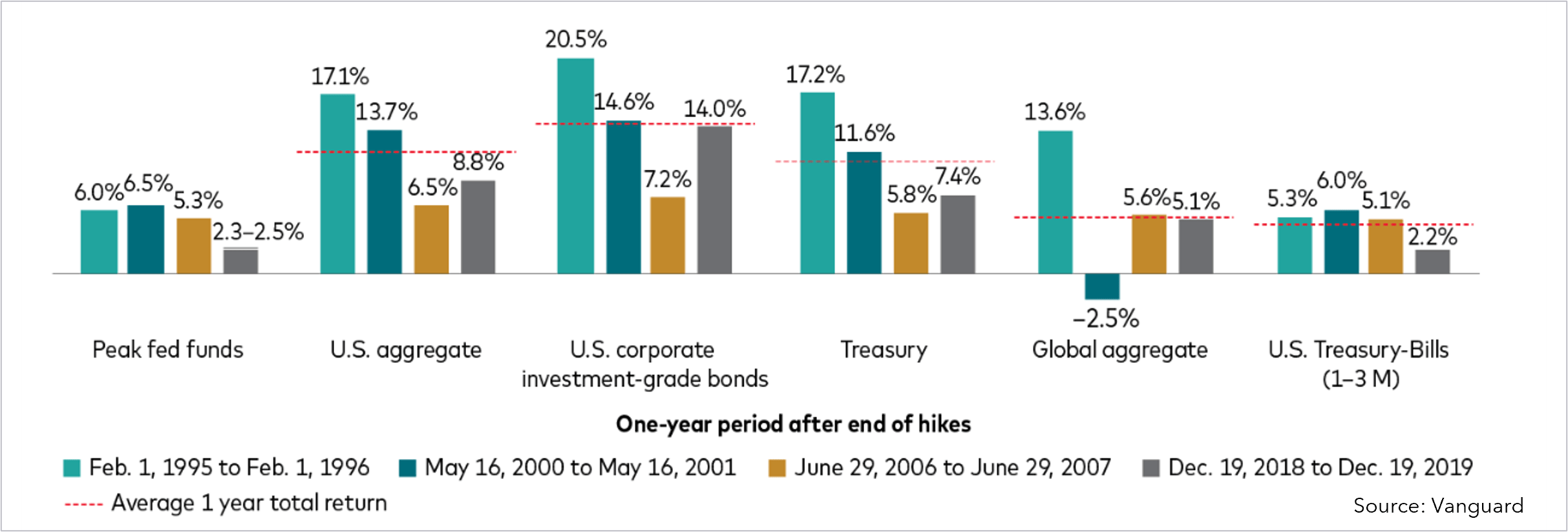

The last decade of zero interest rate policy was essentially a yield desert for investors and to see 5.5% yields on money market funds and Treasury bills (risk free!) is as shiny and alluring as coming upon an oasis after years of seeing even longer-term bonds barely beating inflation.

As welcome as these higher yields are, it is easy for investors to become complacent and assume the current environment will persist, especially with the Federal Reserve chanting the tune of higher for longer rates. Though the timing of a final rate hike in this cycle isn’t certain. What we do know is that the Federal Reserve expects to do just one more rate hike this year and if you look at market expectations for a rate hike as implied by Fed futures, the market doesn’t believe the Federal Reserve will end up hiking again this year.

Are money market funds and Treasury bills the best place to park your money?

Looking at past rate hiking cycles we can see that once the Federal Reserve stops raising rates – generally Treasury bills tend to underperform other segments of the bond market. Although 5.5% yields appear especially attractive today there is likely an opportunity cost of holding onto Treasury bills longer term. That opportunity cost, also called reinvestment risk, is incurred by not beginning to move from money market funds and Treasury bills to longer dated bonds before the Federal Reserve signals it intends to bring rates back down.

In a world with market turbulence and worrisome headlines, it’s crucial to dig deeper and look beyond the surface to gain a more nuanced perspective on the investment landscape. Diversifying beyond the largest mega-cap stocks, considering undervalued international markets, and maintaining a cautious eye on the evolving interest rate landscape can help investors navigate these turbulent times.

1 Source: Goldman Sachs

2 Source: JP Morgan