“We have two classes of forecasters: Those who don’t know – and those who don’t know they don’t know.”

John Kenneth Galbraith

2019 should serve as another reminder that investors should expect the unexpected from the market. It should also, again, call into question the utility of stock market forecasting.

The best summation of 2019 seems to be that it was the opposite of 2018.

As we recall, 2018 started with Wall Street forecasting +9% returns for the S&P 500, with dividends reinvested(1). Instead, it finished -4.4%, punctuated by a -20% price decline to close out the year(2). The market seemed generally concerned that Fed policy was too tight and the trade war too violent(3).

2019 erased those concerns. The Fed got the message(4) while the US and Chinese governments decided to stop throwing sand and play nicer(5). In my view, reversing these headwinds was a big reason the S&P 500 rose +31.49% in 2019.

Where was Wall Street in forecasting this reversal?

The average estimate was +21.4% for 2019, with dividends reinvested. While directionally accurate, it’s less impressive when you consider that it missed by 32.04% and that Wall Street Strategists haven’t collectively forecasted a down year for the past 20 years(6). And their up-year forecasts have missed by wide margins in the past as well(7).

This brings us to this 2020. The Street is calling for an average gain of +3.43%(8). The range is -7.25% to +8.23%. So all-in, they think it’ll be a benign year.

Who wants to bet real money they’re right this time?

Before you wager, remember your chances of being right about as good as the chimps who throw darts for research purposes(9).

The best thing to do when someone sends you a 2020 stock market forecast is to throw it in your fireplace. Then, remind yourself of the historical data and that those thoughtful year-end forecasts are just marketing tools to stay in the press during the holiday slow period. They shouldn’t have much, if any, impact on your long-term financial outcomes.

Instead of starting your year asking what’s the market going to do, ask yourself: “what do I need from the market? And from my overall portfolio?”

As a result, more relevant topics should surface, such as:

- How much income will I need once I’m done working and am I on track to safely achieve it?

- What is an appropriate amount to leave behind to future generations?

- Will those assets be distributed tax-efficiently?

- Do I have a tax-efficient source of money to pay future healthcare expenses?

- Is my portfolio taking too much, or too little, risk?

- What is the appropriate way to measure risk?

- The list goes on…

Once you have a handle on these issues, you’ll know what your future liabilities should be and as a result, you’ll be better informed to allocate your portfolio.

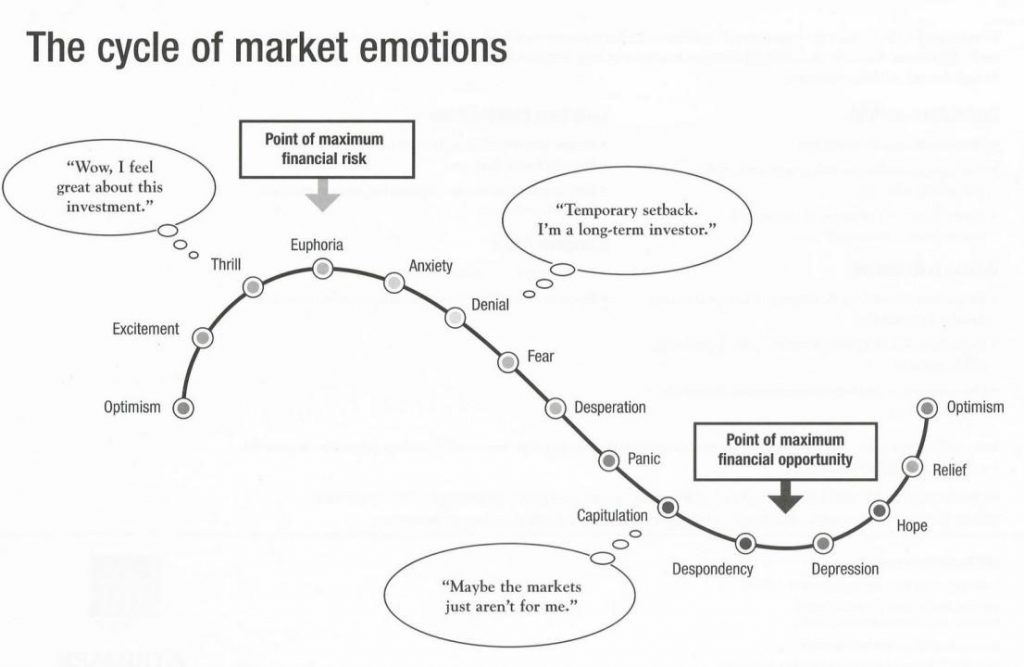

However, if your top priority is to just get more aggressive this year, you may be dealing with a case of FOMO (Fear of Missing Out) based on last year’s market performance. This is normal. Investors expectations of next year’s returns are typically informed by the prior year’s performance(10). Moreover, as we all move farther away from the 2008 financial crisis, our collective financial-PTSD(11, 12, 13) fades a bit more. So ever year that goes by post-crisis, we are a bit more likely to get more aggressive than last year. Provided the past year’s returns were positive, of course.

So, instead of acting on an impulse that tells us to get aggressive at the start of the year, a better exercise would be to do the following:

- Confirm your risk profile, including if you’re unnecessarily seeking or avoiding risk

- Make sure your portfolio allocations are consistent with your long-term funding objectives

- Do nothing – if the first two suggestions check out.

The rest is details. And yes, there are plenty to consider. And they are important. However, before you start going down the path of Roth vs. Traditional, HSA or not, or which of your awesome company benefits to leverage, confirm the big picture is nailed down.

Otherwise, all that time in the weeds might be a waste if the market decides to throw a curve-ball that you’re not prepared for.

And after all, when was the last time that happened?

Sources/Further Reading:

- Lucinda Shen, Will the Stock Market Crash in 2018? Here’s what Wall Street Predicts; Fortune Magazine, December 28, 2017

- S&P Dow Jones Indices; S&P 500 Fact Sheet, December 31, 2019

- Sarah Ponczeik, Vildana Hajric & Luke Kawa; U.S. Stocks Battered by Trade,Yield Concerns: Markets Wrap; Bloomberg; December 3, 2018

- Patti Domm; Powell aces tricky Fed transition to ending interest rate cuts, doing “100% of the right things”; CNBC; October 30, 2019

- Bloomberg News; U.S. Says Phase-One China Deal Would Include Tariff Rollback; November 6, 2019

- Jeff Sommer; Wall Street’s Annual Stock Forecasts: Bullish and Often Wrong; New York Times, December 6, 2016

- Jeff Sommer; Forget Stock Market Forecasts. They’re Less Than Worthless.; New York Times, December 23, 2019

- CNBC Market Strategist Surgery; 2020

- Rick Ferri; Any Monkey Can Beat the Market; Forbes; December 20, 2012

- Hannes Mohrschladt; The Impact of Recency Effects on Stock Market Prices; University of Munster; November 21, 2018

- Bradley T. Klontz, PsyD., CFP and Sonya L. Britt, Ph.D., CFP, Financial Trauma: Why the Abandonment of Buy-and-Hold in favor of Tractical Asset Management May be a Symptom of Posttraumatic Stress; Journal of Financial Therapy – Volume 3, Issue 2, 2012

- Jack Singer; Dr. Jack’s Advice for Advisors: Recognizing PTSD Among Advisors; Financial Advisor Magazine; September 2, 2014

- Nicola Mucci, Gabriele Giorgi, and Giulio Arcangeli; The Correlation Between Stress and Economic Crisis: A Systematic Review; Neuropsychiatric Disease and Treatment; Dove Press; April 21, 2016